IRS Criminal Investigation is the most critical component in maintaining the relatively high U.S. tax compliance rate, the envy of the world and a linchpin of our democratic system. The superb financial investigative abilities of its special agents are an important national security asset when those skills are in demand for other important needs, including terrorist financing matters. Yet the congressional squeeze on the IRS budget is reducing this national asset to a size that endangers its viability.

This article explores that impact. Recent congressional and public pressure to redirect CI resources to identity theft cases and the continuing demand for CI services in combating terrorism and for use in complex international fraud cases like the FIFA corruption case, combined with a dramatic drop in agent resources, are decreasing the resources available to pursue traditional tax fraud cases. The low agent numbers are now at a point that puts retention and the critical roles of training and skills transfer in peril.

Background

CI is the only enforcement agency pursuing investigations of potential criminal violations of the IRC. There are two key aspects of its work from a tax enforcement perspective. First, unlike IRS civil audit activity, CI's cases are public. CI publicizes its cases to send a message far beyond the individual taxpayer being prosecuted — to more than 300 million taxpayers. The message has two components: (1) the threat to those tempted to cheat that there is a great risk to tax evasion, and (2) the assurance to those paying their fair share that they are not chumps and that those not paying it are not getting a free pass, or are at least risking their liberty. Second, the prospect of incarceration is a principal motivator to those tempted to cheat. If the only sanction for tax violations were civil penalties, many more would play the audit lottery more aggressively, especially as congressional budgets drive the audit rate lower each year. Yet even the slight prospect of a loss of liberty in one of our federal correctional institutions causes many to focus when they sign the perjury jurat on their returns.

CI is the most dramatic example of the concept of general deterrence. Tax offenses are the one federal felony that every American confronts each year. We are not all tempted to sell drugs; we are not all in the securities industry or in a position to commit an environmental crime. But we all file returns. Therefore, the IRS must maintain a strong compliance message for the country's 300 million taxpayers, and it has—in recent history, with as few as 1,500 criminal tax prosecutions each year. Even that low number, however, is dropping. That is far below the number of narcotics prosecutions brought by the federal government in attempting to deter a far smaller group of potential violators. Hence, CI needs publicity to achieve even a minimum enforcement presence.

The CI chief, Richard Weber, recently made the same point in a conversation with the author: "Taxpayers voluntarily comply because they know it is the right thing to do, but they also want those who cheat the government to be held accountable. They want a level playing field. When they see that criminals get away with not paying their fair share, there is a direct impact on the voluntary compliance rate and the confidence in our entire system begins to erode. IRS-CI restores that confidence by ensuring that we all play by the same rules."

Declining Resources and New Obligations

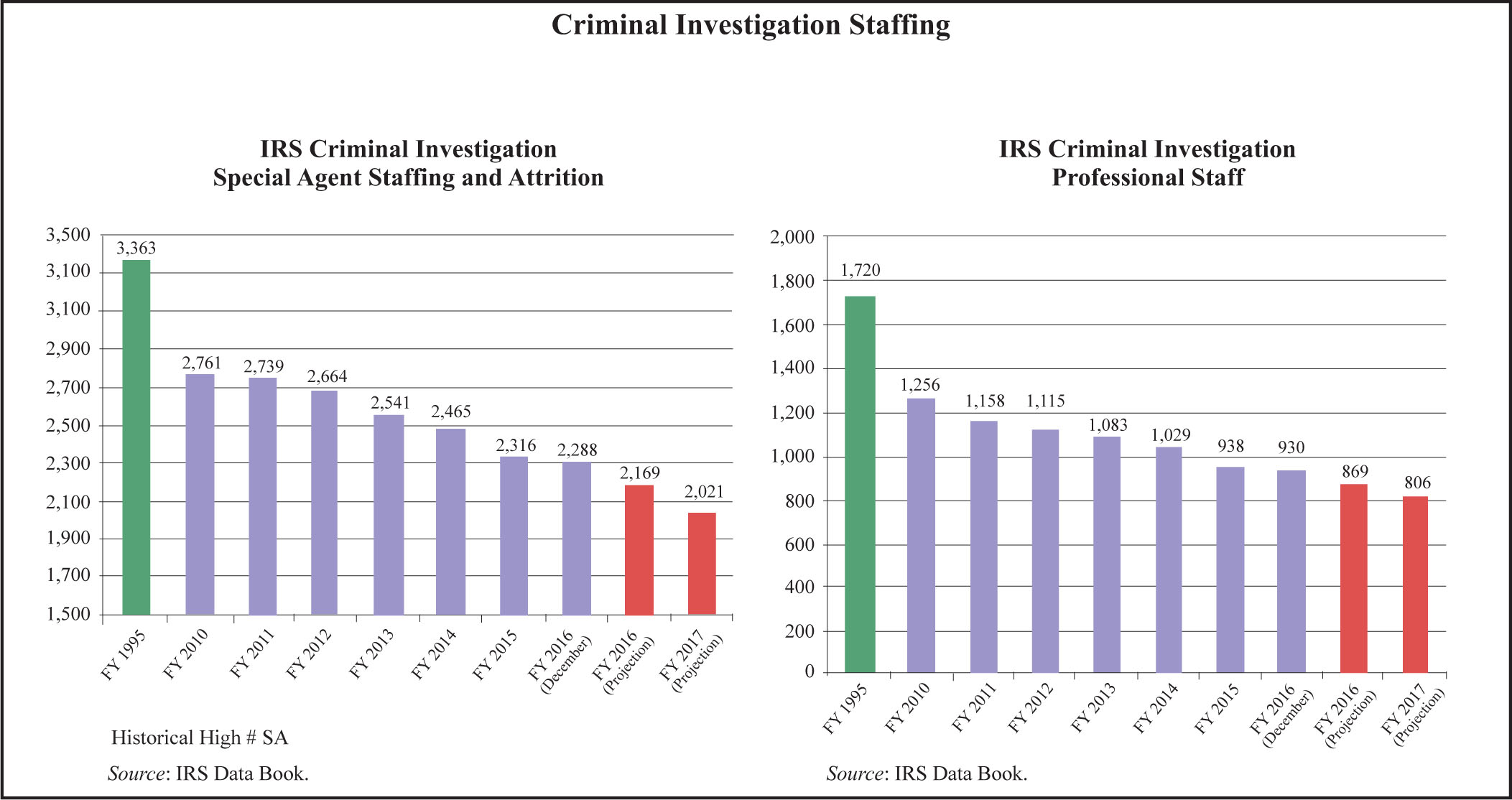

In 1995 CI hit the historical high-water mark in special agent strength: 3,363 agents. When I had the privilege of leading CI, that number had fallen below 3,000; the current level is 2,288. Worse, the already built-in budget declines indicate agent strength will likely fall to 2,000 agents by 2017 and below 2,000 thereafter. At the same time, the professional staff has fallen from 1,720 to less than 900.

Criminal investigations inevitably involve intensive and detailed individual agent time and significant management oversight — as we all would want. Despite best efforts, it's difficult to automate or make dramatic efficiency gains in those investigations. In the civil arena, the IRS has made great gains in efficiency with electronically filed returns, automated correspondence exams, and automatic underreporter programs, for example. But that simply cannot and should not be attempted in a criminal context.

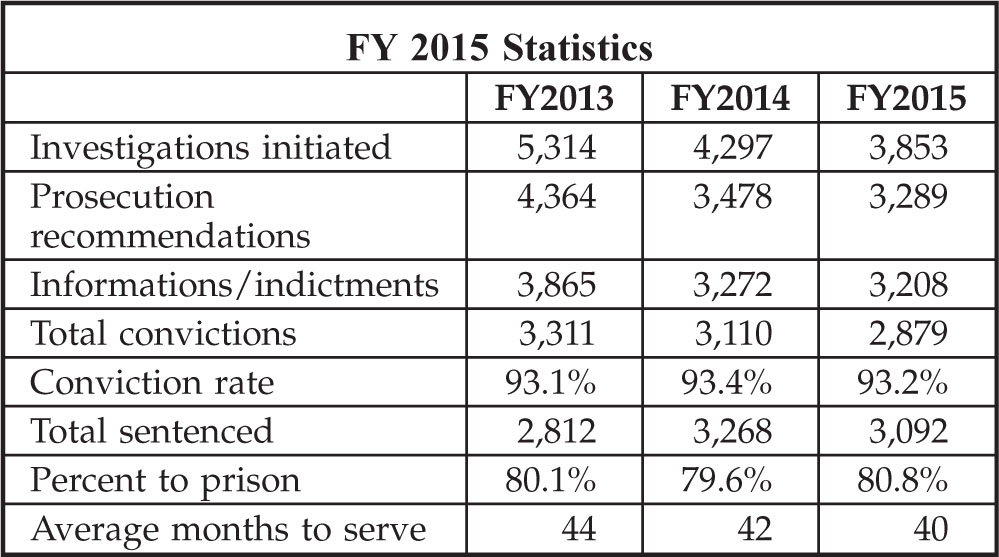

The inevitable result of CI budget declines is a decline in CI's core product—criminal cases and convictions. The most recent enforcement statistics released by the IRS show the number of investigations initiated dropping from 5,314 in 2013 to 3,853 in 2015 and convictions dropping from 3,865 to

3,208. But even those numbers mask the true drop in tax cases. Those numbers include not only tax and tax-related matters but also other categories of cases: money laundering, narcotics, terrorist financing, and identity theft, which has grown massively. While it is true that CI is reimbursed through the Organized Crime Drug Enforcement Task Forces program for most of its money-laundering- and narcotics-related work, there has been no increase in resources to deal with the explosion in identity theft cases.

CI has included the more than 1,000 identity theft cases in recent years in the tax and tax-related categories of cases even though they relate to tax in only the broadest sense. There are no tax issues in those cases; the wrongdoings at issue are pure fraud schemes. No experts would conclude that identity theft cases advance traditional tax enforcement. Those cases are directed at a form of "street white-collar" crime, and they do nothing to deter average citizens from considering tax evasion. They do, however, respond to the obvious public and congressional concern about identity theft. There is little that is more frustrating than learning your refund has been stolen by some unknown criminal. While that is important work, the IRS should either get additional resources from Congress to do it or use other law enforcement agencies to do it until a systematic fix is in place.

The declining numbers mask yet further damage to this valuable government workforce. When special agent numbers drop this low, it is difficult to maintain a consistent recruitment program and even harder to maintain an effective training program. When I was CI chief, we ran as many as 12 training classes per year at the Federal Law Enforcement Training Centers. Now they are lucky to have a class or two annually. That leads to degradation in the all-important training environments. Moreover, because special agents are eligible to retire as early as age 50, CI loses many of its most experienced and skilled agents each year. As the numbers drop, the number of agents and the amount of time available for field-level training diminish. There are many of us who already doubt whether the IRS could still conduct an old net-worth-type prosecution, and no one has seen one in years. Those are valuable skills that the agency is losing.

Given the increasingly international nature of the cases CI works, such as the recent offshore banking cases or a case like FIFA's, CI must station agents abroad. If the Foreign Account Tax Compliance Act and the common reporting standard work, there will be an even greater need for CI's boots on the ground abroad, but the budget trends will not allow that.

Another challenging development for all law enforcement, but particularly CI given the role of computers in the crimes it pursues, is the need to have sufficient agents trained in a cyber environment. As Weber described it to the author: "As criminals continue to become more sophisticated in the way that they defraud the government, we must do all we can to stay one step ahead of them. Cyber platforms are the new playing field for today's criminals. We must invest in the tools to ensure that the country's best financial investigators are properly trained and equipped to do battle with today's criminals in the cyber world—whether it is a complex tax case, sophisticated stolen identity refund fraud case, or a terrorist financing case, IRS-CI needs to lead this effort to ensure that taxpayers can have confidence in their financial system."

The Enforcement-Deterrence Impact

CI already struggles to maintain a consistent enforcement message in multiple media outlets. It maintains a significant and detailed presence on the IRS website featuring data and summaries of publicly available information on hundreds of convictions, separated by various subprogram categories

(https://www.irs.gov/uac/Criminal-Enforcement-Statistical-Data). But it needs to get these criminal convictions reported not only in the tax press and national papers but also in local newspapers, on websites, and in nightly news reports. That is where the enforcement battle is really won — in hundreds of regional newspapers and local television markets.

To maintain a reasonable coverage in 50 separate states and hundreds of distinct media markets, CI should be bringing thousands of cases each year. If you start with 3,853 total investigations being initiated in 2015 but eliminate identity theft cases (776), narcotics cases (955), and money-laundering cases

(1,436), you reach a number reflecting that very few traditional tax cases are being initiated — even if you concede there is some double counting in those numbers. The IRS statistics report 1,202 general tax fraud case initiations in fiscal 2015, but when you consider that in recent years only about two-thirds of the initiations have been prosecuted, you see that traditional tax cases prosecuted per year have dropped significantly. Plus, some of those cases fall into other program areas like healthcare fraud and bankruptcy fraud. The number of traditional criminal tax cases being pursued—when the only violation involved is a tax crime—has fallen to a dangerously low level.

Loved Too Much

One of CI's biggest historical issues is that the agents and their skills are sought after for so many different roles. It seems that every decade or so, there is a blue-ribbon study of the IRS, and each time it bemoans the shifting of CI resources to other investigative priorities. The most recent report in 1999, known as the Webster Commission report, described this as "mission drift" and strongly urged the IRS commissioner to put CI back in the tax enforcement business.

The largest unreimbursed non-tax-related drain on CI's resources is identity theft cases. As indicated above, in recent years, CI has initiated more than 1,000 such cases each year, and those cases have consumed as much as 18 to 20 percent of an agent's time available for investigative work on average. The good news is that there were only 776 cases initiated in fiscal 2015, and CI tries to work these cases in conjunction with other law enforcement agencies, reducing the drain on special agent resources. This is one of those areas in which Congress wants to have it both ways—speedy refunds and no fraud. Yet the two demands are in direct competition with each other: The faster the refund, the fewer the anti-fraud checks and controls. Hopefully, the IRS will develop and implement changes in the fraud detection systems that will catch more of that activity before refunds are issued. Alternatively, those cases—if so important to the public and to Congress—should be a key basis for additional funding for CI.

National Security Imperative

If you are not already convinced that the tax enforcement mission is important enough to save CI, there is another compelling reason. Unknown to many is the critical role IRS special agents play when the best financial investigative skills are needed in the world of terrorist financing cases. I was the chief of CI on September 11, 2001, and within a few hours of the terrorist attacks, we received a request from an individual very high up in the U.S. national security establishment for special agents to be on the ground in the Middle East immediately to start following the money trail. We asked for six volunteers and, as you would expect, received too many responses. One of these days, maybe we can tell the story about where they went and what they did.

Another little-known fact is that more than 100 special agents volunteered to serve and did serve as air marshals after 9/11, even though that work was pretty far afield from the mission for which they signed up. During the Hurricane Katrina flooding, it was the special agents who remained at or actually moved toward flooding IRS offices to secure them as much as possible. IRS Commissioner Charles O. Rossotti referred to them as the "marines of the IRS," and that always seemed to capture it perfectly.

For all the reasons stated above, Congress should not allow this talented and critical group of agents to wither to numbers that eviscerate their worth to our country. Too much is at stake. The maintenance of our still-laudable tax compliance rate is essential to our functioning democracy. CI (and a fully funded IRS) is a relatively small price to pay. If our compliance rate started to fall because of perceived lack of enforcement, it would be much more expensive (and painful) to restore the status quo.

Mark E. Matthews is a member of Caplin & Drysdale, Chtd. He has served in several senior tax administration positions at the Treasury and Justice departments, including chief of the IRS Criminal Investigation division, IRS deputy commissioner for services and enforcement, and deputy assistant attorney general. Matthews explains how recent congressional budget cuts are damaging the effectiveness and long-term vitality of the IRS's criminal tax enforcement capacity, and he discusses the critical tax deterrence message CI must maintain.

This article was originally published in the March 14, 2016, issue of Tax Notes, a publication of Tax Analysts © 2016.